Initiating Coverage | Auto Ancillary

March 13, 2015

Setco Automotive

BUY

CMP

` 242

MHCV upcycle to stoke growth

Target Price

` 286

Setco Automotive Ltd (SAL) which is the market leader in manufacture of MHCV

Investment Period

12 Months

clutches (about 65% market share) is likely to reap rich benefits of upcycle in both

the OEM (30% of sales) as well as replacement markets (70% of sales).

Stock Info

Direct beneficiary of MHCV upcycle

Sector

Auto Ancillary

After two consecutive years (FY2013 and FY2014) of a steep double-digit decline,

Market Cap (` cr)

646

the MHCV segment is on course for a cyclical upturn. The uptrend is clearly visible

with the segment reporting a growth of 13% in YTD FY2015 (April 2014 to

Net Debt (` cr)

173

January 2015). We believe the MHCV segment is well poised to maintain the

Beta

0.9

double-digit growth over the FY2015-FY2017 period due to a) Better economic

52 Week High / Low

294 / 68

outlook which is likely to generate freight revenues, b) Firming of freight rates and

Avg. Daily Volume

12,735

improvement in fleet operators’ profitability, c) Expected reduction in interest rates

which would revive the investment cycle, and d) Budgetary focus to increase road

Face Value (`)

10

network which would enhance usage of commercial vehicle (CV)s. SAL would be the

BSE Sensex

28,503

direct beneficiary of uptick in MHCV OEM demand as it commands 85% market

Nifty

8,648

share, drawing about 30% of its total revenues from the space.

Reuters Code

SETC.BO

Aftermarket and export focus to be growth drivers

Bloomberg Code

SETC@IN

Improved fleet utilization due to higher freight availability is likely to propel the

replacement demand for clutches. SAL previously used to cater to replacement

market only through the OEM authorized distribution channels. However, SAL is

Shareholding Pattern (%)

now teaming up with multi branded distributors (network partners other than the

Promoters

63.0

OEM authorised outlets) to independently tap the replacement market. These

distribution channels provide huge opportunity as SAL can effectively tap the third

MF / Banks / Indian Fls

3.8

and fourth replacement cycle for clutches which are typically done outside the

FII / NRIs / OCBs

18.4

OEM authorized dealerships. We expect SAL aftermarket segment to post a CAGR

Indian Public / Others

14.8

of ~18% over the next two years. Also, SAL is negotiating with American and

European OEM’s to commence supplies to their authorized aftermarket channels.

SAL is already supplying to these OEMs in India and is now aiming to initiate

Abs. (%)

3m 1yr 3yr

supplies to their overseas arms. We expect exports (contributing about 9% of the

revenues) to register a healthy 25% CAGR over the FY2015-FY2017.

Sensex

4.2

30.9

60.0

Setco

(3.2)

240.8

103.9

Outlook and valuation: SAL is likely to clock a 24% CAGR in revenues over the

next two years given the improvement in the MHCV OEM space and market share

gains in the replacement segment. Also, SAL’s operating margin is also expected

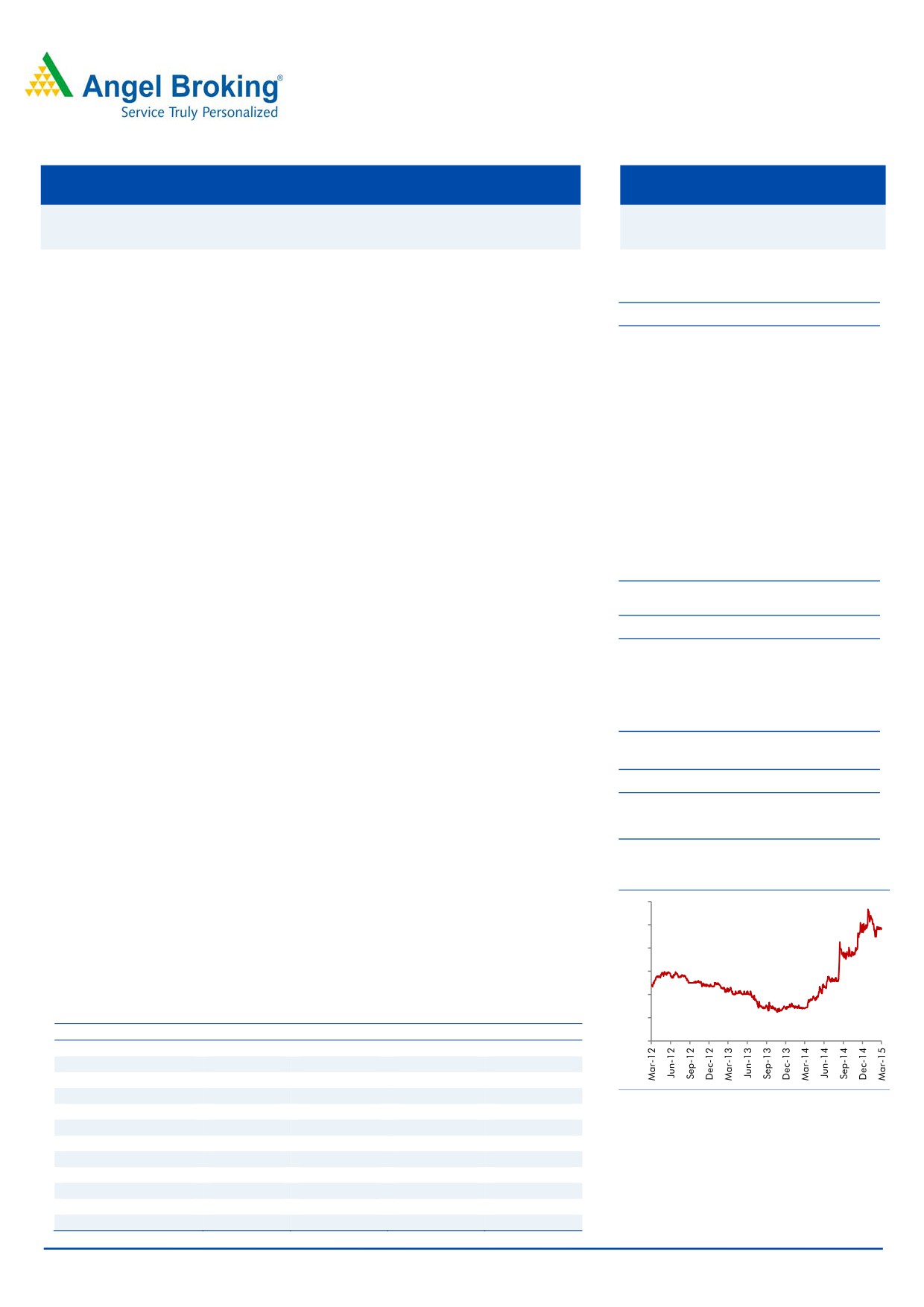

3-Year Daily price chart

to improve by 200bp over the next two years, given the operating leverage,

300

enhanced capacity utilization and procurement of captive castings. Given the healthy

250

top-line growth and margin improvement, SAL is expected to post a robust 49%

CAGR in earnings. SAL’s return ratios are also likely to expand due to improved

200

profitability and moderate capex. We initiate coverage on the stock with a Buy

150

recommendation and target price of `286 (based on 15x FY2017E earnings).

100

Key financials

50

Y/E March (` cr)

FY2014

FY2015E

FY2016E

FY2017E

0

Net sales

390

565

718

862

% chg

(2.4)

45.0

27.0

20.0

Net profit (Adj.)

11

23

36

51

% chg

(59.6)

115.9

56.4

42.5

Source: Company, Angel Research

EBITDA margin (%)

9.7

12.3

13.3

14.3

EPS (`)

4.0

8.5

13.4

19.0

P/E (x)

61.2

28.3

18.1

12.7

P/BV (x)

3.4

3.2

2.8

2.4

RoE (%)

5.6

11.2

15.4

18.6

RoCE (%)

9.0

12.3

15.1

17.4

Bharat Gianani

EV/Sales (x)

1.5

1.1

1.0

0.8

022-39357800 Ext: 6817

EV/EBITDA (x)

15.9

9.3

7.2

5.9

Source: Company, Angel Research, Note: CMP as of March 13, 2015

Please refer to important disclosures at the end of this report

1

Setco Automotive | Initiating Coverage

Investment Arguments

SAL to be direct beneficiary of MHCV upcycle

After two consecutive years of double-digit decline (FY2013 and FY2014), the

MHCV segment has resurged in FY2015. During the April 2014-December 2014

period, the segment registered a healthy growth of 13%. Improvement in the

MHCV segment can be attributed to a) Better economic growth, given the reform

driven policies of the government, b) Firming of freight rates and improved freight

availability, c) Reduction in diesel prices and lower inflation leading to

improvement in operating metrics of fleet operators, and d) Reduction in interest

rates.

Macro-economic indicators have turned favourable and we expect economic

growth to accelerate, going ahead. Further, the government’s thrust on

infrastructure (development of road network) would indirectly boost demand for

MHCVs. We believe the MHCV segment has resumed its uptrend and is well

poised to maintain double digit growth momentum over the next two years

(FY2015-FY2017). SAL would stand to be a direct beneficiary of the revival in the

MHCV OEM space as it derives about 30% of its revenues from this segment.

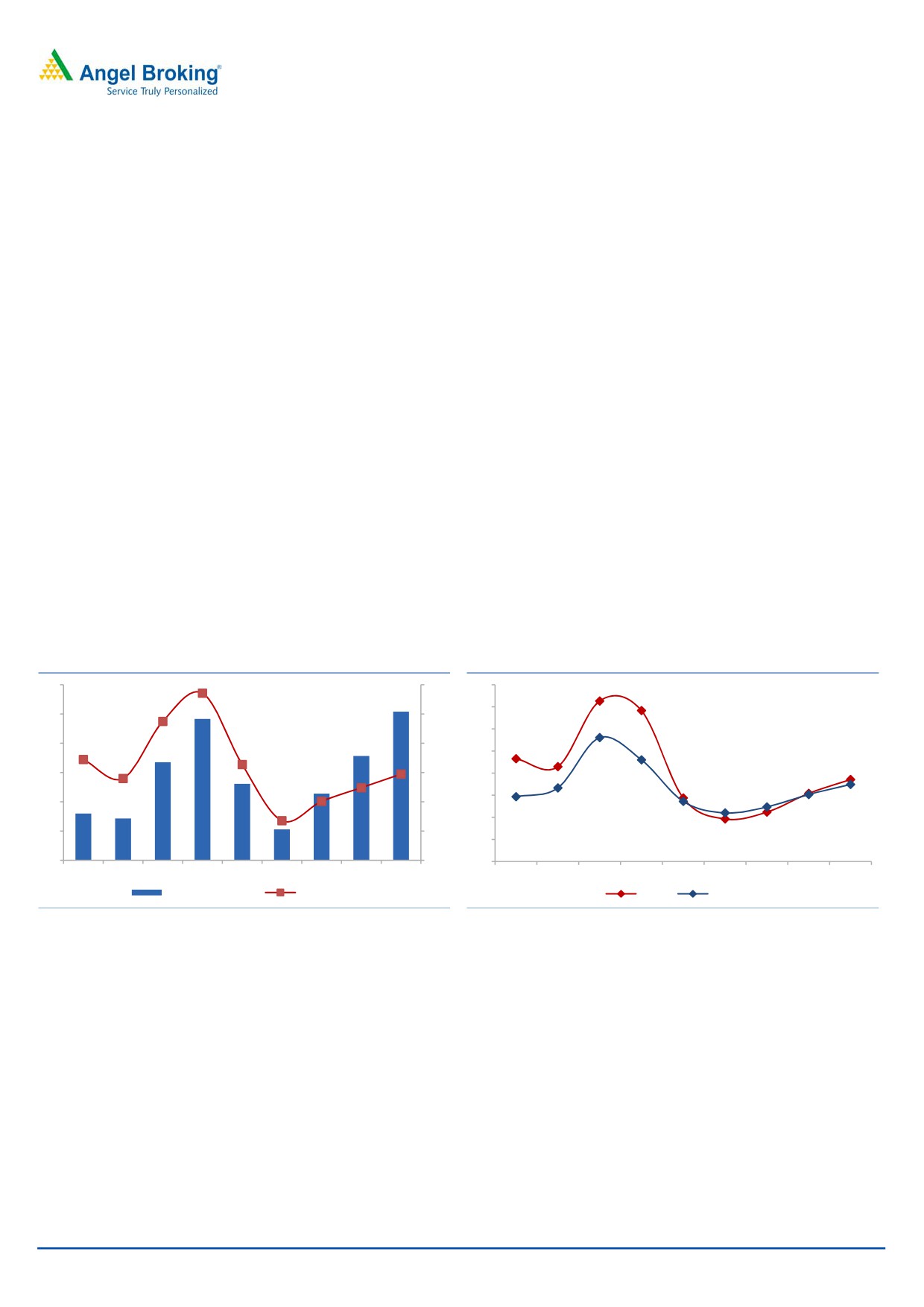

Exhibit 1: MHCV industry growth trends

4,50,000

50

4,00,000

40

3,50,000

30

3,00,000

20

2,50,000

10

2,00,000

0

1,50,000

(10)

1,00,000

(20)

50,000

(30)

0

(40)

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

MHCV Industry

Growth %

Source: SIAM, Angel Research

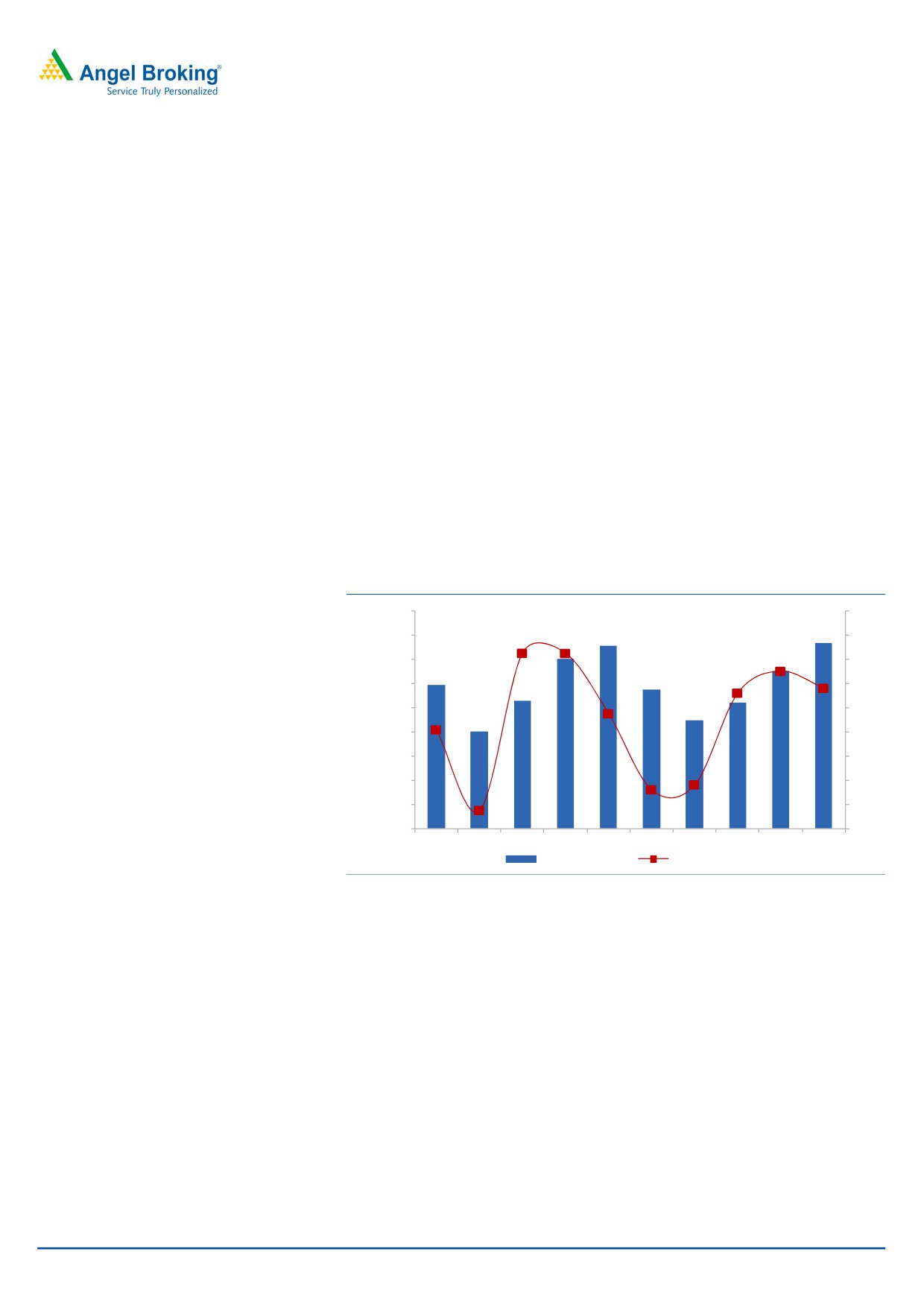

Improvement in replacement demand and independent

aftermarket channel to fuel growth

Improved economic outlook and better freight availability are likely to spur

capacity utilization of the freight operators. Increased usage of vehicles would

boost replacement demand over the next two years. As per industry estimates, the

market size of the replacement segment is about 3x the size of the OEM segment.

In addition to sales through the OEM aftermarket network, SAL has tied up with

multibranded distributors (touch points other than OEM authorized channels). SAL

previously used to cater to replacement market only through the OEM authorized

distribution channels. SAL is, thus independently tapping the replacement space.

We believe this strategy provides a huge opportunity to SAL as it would enable the

company to effectively tap the third and the fourth replacement cycle of the clutch

(beyond five years of the vehicle age). This would be considering that replacements

March 13, 2015

2

Setco Automotive | Initiating Coverage

for such aged vehicles are typically carried outside the OEM’s authorised

aftermarket channels. SAL commenced its independent network in September

2013 and has already realized 10% of the revenues through this network. We

believe this strategy provides SAL with a huge untapped opportunity and would

likely fuel growth. We estimate SAL’s aftermarket revenues to grow at robust 18%

CAGR over FY2015-2017 period.

Exhibit 2: SAL after market growth trend

(` cr)

600

500

400

300

200

100

0

FY10

FY11

FY12

FY13

FY14

FY15E

FY16E

FY17E

Source: Company, Angel Research

Focus on exports provides another growth lever

SAL is focusing on enhancing exports by tapping the replacement markets

overseas. To boost exports, it is focusing on three key markets viz America, Europe

and Africa. The company has developed a new product (Angular spring) for the US

markets, for which the supplies would commence from the beginning of FY2016.

SAL is targeting revenues of `150cr from the US over the next three years. Also,

SAL is in talks with the European OEMs - MAN and Bharat Benz, for the supply of

clutches through their aftermarket channels. SAL is already supplying clutches

through their aftermarket network in India and is hopeful of tapping the European

replacement segment. Apart from US and Europe, SAL is also aggressively tapping

the African market given that most of the trucks are of European make, for which,

SAL already has a product. We expect SAL export revenues to grow at healthy

CAGR of 25% over the next two years

March 13, 2015

3

Setco Automotive | Initiating Coverage

Exhibit 3: SAL export growth trend

(` cr)

60

50

40

30

20

10

0

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Source: Company, Angel Research

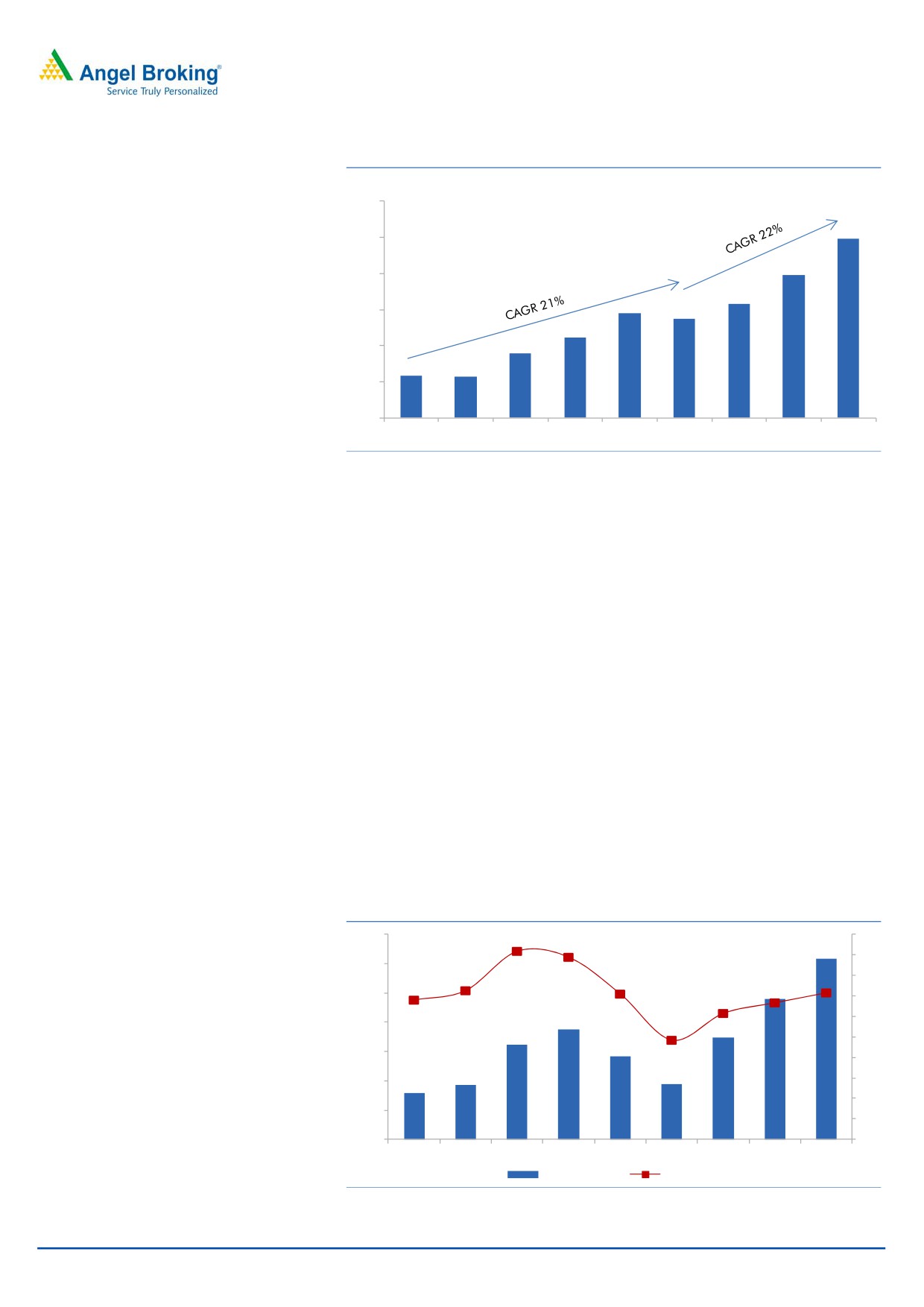

Operating leverage coupled with backward integration to

enhance margins

SAL’s revenues are likely to grow at a CAGR of 24% over FY2015-FY2017 given

the upcycle in the MHCV OEM segment and healthy growth in the replacement

market due to economic revival and with the company setting up an independent

network. Further, SAL is currently operating at capacity utilization of about 65%.

SAL is likely to realize benefits of operating leverage given the uptick in volumes

and higher capacity utilization.

Also, SAL has entered into a JV with Lingotes Especiales S.A., a Spanish firm, for

the manufacture of machined castings which are critical in the manufacture of

clutches. The JV has planned to incur a capex of `150cr and production is slated

to commence in March 2015. About 35% of the production would be used for

SAL’s captive consumption and the remaining would be sold outside. Apart from

margin improvement due to captive production, SAL would also benefit from timely

procurement. We expect SAL’s margins to improve by about 200bp over the next

two years.

Exhibit 4: EBIDTA margin trend

140

20

18

120

16

100

14

12

80

10

60

8

40

6

4

20

2

0

0

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

EBIDTA (` cr)

Margin (%)

Source: Company, Angel Research

March 13, 2015

4

Setco Automotive | Initiating Coverage

Increased supplies to LCV and farm equipment segment provides

diversification

SAL derives more than 90% of its revenues from the MHCV segment. The MHCV

segment is cyclical in nature having direct relation with economic growth. Any

slowdown in the economy impacts freight availability, thereby leading to negative

sentiments and steep decline in MHCV sales (sales have declined in double-digits

in the previous down cycles). In order to diversify and reduce volatility in revenues,

SAL is increasing supplies to the less cyclical LCV and farm equipment segments.

SAL can easily scale up presence in the LCV space given that most of its existing

customers viz Tata Motors, Ashok Leyland, Eicher are already present in the LCV

segment and SAL has well established relations with these OEMs. To further

diversify, SAL would also commence supplies to the tractor segment.

Improving margins and capacity utilization to boost return ratios

SAL’s margins are likely to improve by 200bp over FY2015-17 on back of

operating leverage and backward integration. Further, capacity utilization levels

would also increase from about 65% currently to about 90% levels by FY2017.

Also, SAL has no major capex lined up over the next two years, which would

augment the asset turnover ratios. These factors are expected to boost the return

ratios. RoE is expected to improve from 11% in FY2015 to 19% levels in FY2017.

Similarly the RoCE is expected to improve from 12% in FY2015 to 17% in FY2017.

Exhibit 5: Net Profit and margin trend

Exhibit 6: Return ratios

60

12

40

35

50

10

30

40

8

25

30

6

20

15

20

4

10

10

2

5

0

0

0

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Net Profit (` cr)

Margin %

RoE%

RoCE%

Source: Company, Angel Research

Source: Company, Angel Research

Outlook and Valuation

SAL is likely to clock a 24% CAGR in revenues over the next two years. Revenues

are expected to be driven by an upcycle in the MHCV OEM segment, coupled with

the company setting up independent aftermarket outlets, and with the company’s

increased focus on exports. Further, the joint venture with Lava Cast for casting

supplies provides additional growth prospects to the company. SAL’s operating

margin is also expected to improve by 200bp over the next two years, given the

operating leverage, enhanced capacity utilization and procurement of captive

castings. Given the healthy top-line growth and margin improvement, SAL is

expected to post a robust 49% CAGR in earnings. SAL’s return ratios are also likely

to expand due to improved profitability and moderate capex. We initiate coverage

on the stock with a Buy recommendation and target price of `286 (based on 15x

FY2017E earnings).

March 13, 2015

5

Setco Automotive | Initiating Coverage

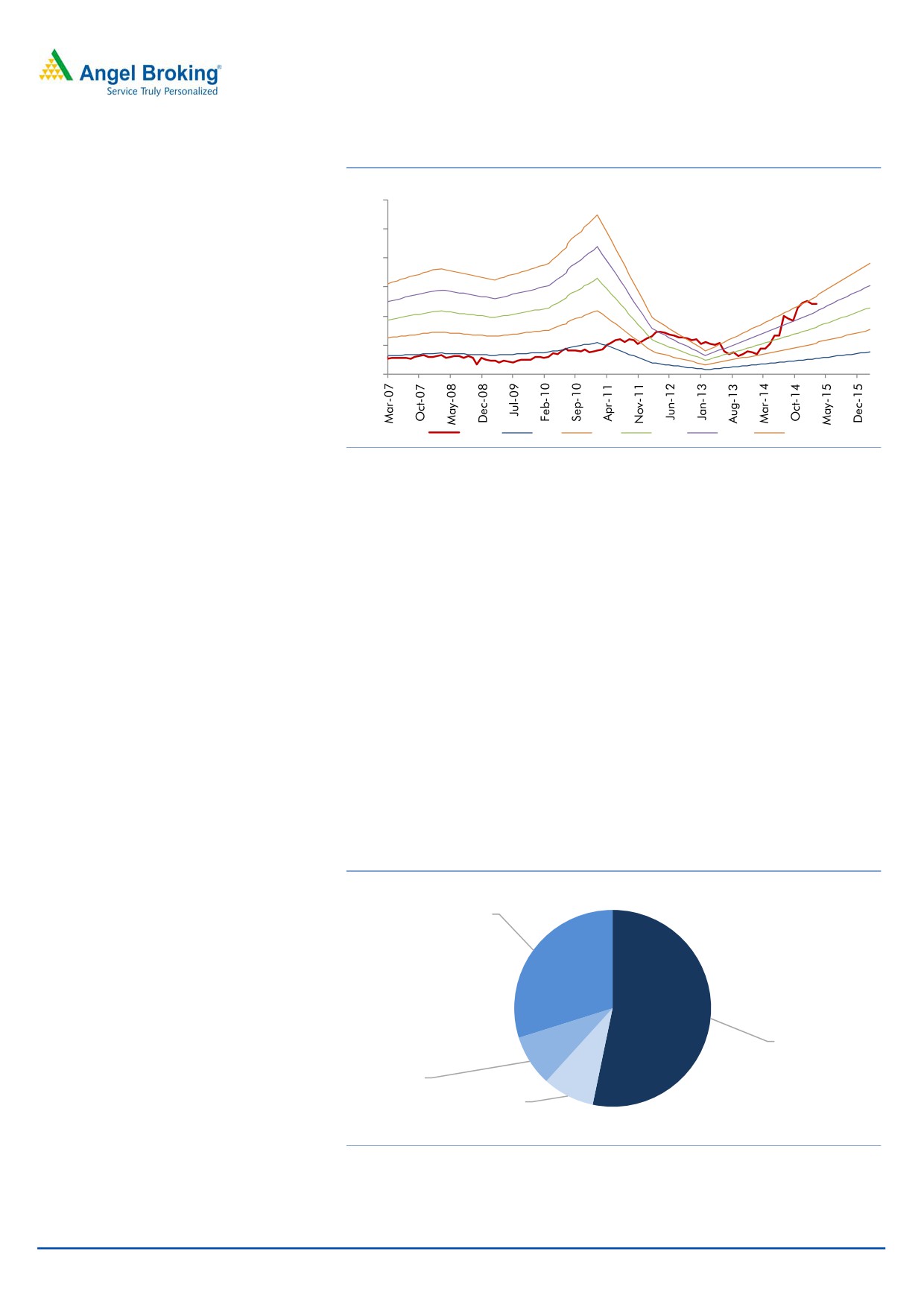

Exhibit 7: One-year forward P/E band

(`)

600

500

400

300

200

100

0

Price

4x

8x

12x

16x

20x

Source: Company, Angel Research

Company Background

Setco Automotive Ltd (SAL) is the largest manufacturer of clutches for commercial

vehicles. The company has a market share of 85% in the MHCV OEM segment,

supplying to majors like Tata Motors, Ashok Leyland, Volvo-Eicher, Bharat Benz,

Asia Motor Works and Mahindra & Mahindra. In the MHCV replacement segment,

SAL has a market share of about 65%. SAL’s products are sold under the “Lipe”

brand. It has four manufacturing facilities; two in India (Gujarat and Uttarakhand)

and one each in the US and the UK. Apart from commercial vehicles, SAL also

manufactures clutches for hydraulic products used in the construction equipment

industry and precision engineering components.

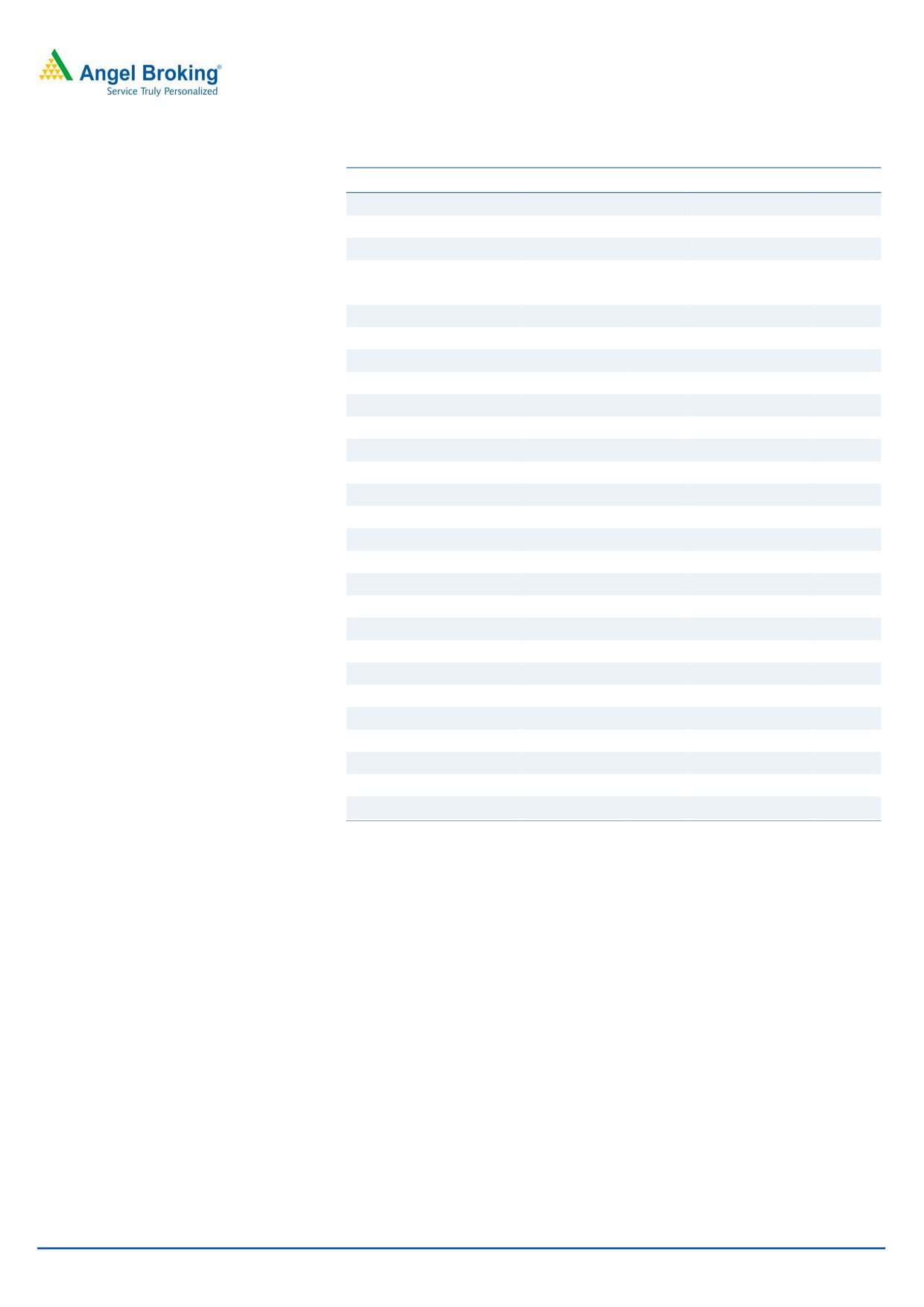

The replacement segment is the largest contributing segment accounting for about

62% of the overall revenues. Aftermarket sales through the OEM channel contribute

53% of the revenue while sales through the independent route contribute 9%. OEM

sales form 30% of the overall revenues while exports account for 9%.

Exhibit 8: Segment wise revenue break up

OEM, 30%

Aftermarket

(OES), 53%

Exports, 8%

Aftermarket

(Independent),

9%

Source: Company, Angel Research

March 13, 2015

6

Setco Automotive | Initiating Coverage

Profit & Loss Statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Total operating income

423

399

390

565

718

862

% chg

19.9

(5.6)

(2.4)

45.0

27.0

20.0

Total Expenditure

348

343

352

496

623

739

Net Raw Materials

241

222

219

312

393

467

Personnel

40

46

52

70

83

98

Other

66

74

81

114

146

174

EBITDA

75

57

38

70

96

123

% chg

16.0

(24.7)

(33.4)

84.2

37.7

28.8

(% of Net Sales)

17.8

14.2

9.7

12.3

13.3

14.3

Depreciation & Amortisation

11

12

14

16

19

21

EBIT

68

49

34

53

77

102

% chg

20.0

(27.3)

(31.8)

58.8

44.7

32.7

(% of Net Sales)

16.0

12.3

8.6

9.4

10.7

11.9

Interest & other Charges

19

20

23

27

32

38

Other Income

3

5

9

12

14

16

PBT (recurring)

49

29

10

27

45

64

% chg

11.0

(39.8)

(65.4)

162.8

68.3

42.5

Extraordinary Expense/(Inc.)

(3)

0

8

0

0

0

PBT (reported)

46

29

18

27

45

64

Tax

1

3

0

4

9

14

(% of PBT)

1.3

11.2

(3.5)

15.0

21.0

21.0

PAT (reported)

45

26

18

23

36

51

ADJ. PAT

48

26

11

23

36

51

% chg

44.0

(45.9)

(59.6)

115.9

56.4

42.5

(% of Net Sales)

11.4

6.5

2.7

4.0

5.0

5.9

Basic EPS (`)

25.8

9.8

6.8

8.5

13.4

19.0

Fully Diluted EPS (`)

27.4

9.8

4.0

8.5

13.4

19.0

% chg

44.0

(64.2)

(59.6)

115.9

56.4

42.5

March 13, 2015

7

Setco Automotive | Initiating Coverage

Balance sheet statement

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

18

27

27

27

27

27

Reserves& Surplus

115

155

163

177

205

247

Shareholders Funds

133

182

189

204

231

274

Total Loans

142

173

178

220

270

305

Deferred Tax Liability

6

7

7

7

7

7

Other long term liab.

-

-

-

-

-

-

Long term provisions

1

1

1

1

1

1

Total Liabilities

282

362

375

432

509

587

APPLICATION OF FUNDS

Gross Block

154

202

230

270

310

350

Less: Acc. Dep.

52

65

80

97

115

136

Net Block

103

137

150

174

195

214

Capital WIP

12

14

8

8

8

8

Investments

22

37

51

61

68

74

Loans and adv.

33

40

46

56

72

86

Current Assets

207

214

216

270

344

416

Cash

9

3

5

5

7

6

Other

177

191

189

233

298

363

Current liabilities

74

59

75

106

138

164

Net Current Assets

133

155

141

164

206

252

Total Assets

282

362

375

432

509

587

March 13, 2015

8

Setco Automotive | Initiating Coverage

Cash flow statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

Profit before tax

46

29

18

27

45

64

Depreciation

16

13

15

16

19

21

Change in Working Capital

(39)

(28)

17

(23)

(41)

(47)

Others

2

1

0

(0)

0

0

Direct taxes paid

(1)

(3)

0

(4)

(9)

(14)

Cash Flow from Operations

24

13

51

16

14

25

(Inc.)/ Dec. in Fixed Assets

(32)

(49)

(22)

(40)

(40)

(40)

(Inc.)/ Dec. in Investments

(13)

(15)

(15)

(10)

(7)

(6)

(Inc.)/ Dec. in Loans & Adv

(7)

(7)

(6)

(0)

(7)

(6)

Cash Flow from Investing

(52)

(72)

(43)

(50)

(54)

(52)

Issue of Equity

0

9

0

0

0

0

Inc./(Dec.) in loans

38

31

5

42

50

35

Dividend Paid (Incl. Tax)

(8)

(8)

(8)

(8)

(8)

(8)

Others

4

22

(2)

0

0

0

Cash Flow from Financing

34

53

(5)

34

42

27

Inc./(Dec.) in Cash

5

(6)

2

0

2

(1)

Opening Cash balances

4

9

3

5

5

7

Closing Cash balances

9

3

5

5

7

6

March 13, 2015

9

Setco Automotive | Initiating Coverage

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

8.8

24.7

61.2

28.3

18.1

12.7

P/CEPS

7.2

16.8

26.7

16.5

11.9

9.0

P/BV

3.2

3.6

3.4

3.2

2.8

2.4

Dividend yield (%)

1.7

1.1

1.1

1.3

2.1

2.9

EV/Sales

1.3

1.5

1.5

1.1

1.0

0.8

EV/EBITDA

7.5

10.5

15.9

9.2

7.2

5.9

EV / Total Assets

2.0

1.6

1.6

1.5

1.4

1.2

Per Share Data (`)

EPS (Basic)

27.4

9.8

4.0

8.5

13.4

19.0

EPS (fully diluted)

27.4

9.8

4.0

8.5

13.4

19.0

Cash EPS

33.5

14.4

9.1

14.6

20.3

26.9

DPS

4.0

2.7

2.7

3.2

5.0

7.1

Book Value

75.5

68.2

71.0

76.5

86.7

102.7

Dupont Analysis

EBIT margin

16.0

12.3

8.6

9.4

10.7

11.9

Tax retention ratio

1.0

0.9

1.0

0.9

0.8

0.8

Asset turnover (x)

1.5

1.1

1.1

1.3

1.4

1.5

ROIC (Post-tax)

24.5

12.2

9.4

10.6

12.1

13.9

Cost of Debt (Post Tax)

13.0

10.2

13.6

10.2

9.4

9.8

Leverage (x)

1.0

0.9

0.9

1.1

1.1

1.1

Operating ROE

35.9

14.0

5.6

11.0

15.3

18.4

Returns (%)

ROCE (Pre-tax)

24.0

13.6

9.0

12.3

15.1

17.4

Angel ROIC (Pre-tax)

24.8

13.7

9.1

12.5

15.4

17.6

ROE

36.3

14.4

5.6

11.2

15.4

18.6

Turnover ratios (x)

Asset Turnover (Gross Block)

2.7

2.0

1.7

2.1

2.3

2.5

Inventory / Sales (days)

76.7

101.5

111.7

88.7

89.4

91.6

Receivables (days)

76.4

72.6

65.4

62.0

62.0

62.0

Payables (days)

63.5

53.7

70.1

68.4

70.2

69.4

WC cycle (ex-cash) (days)

107.4

139.1

126.9

102.3

101.2

104.2

Solvency ratios (x)

Net debt to equity

1.0

0.9

0.9

1.1

1.1

1.1

Net debt to EBITDA

1.8

3.0

4.6

3.1

2.7

2.4

Interest Coverage (EBIT / Int.)

3.6

2.5

1.4

2.0

2.4

2.7

March 13, 2015

10

Setco Automotive | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal approval

from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates

including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by

Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of

the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or employee of

company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Setco Automotive

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

March 13, 2015

11